GLM 5.2 Reaches Accountant-Level Accuracy, AI Starts Taking On Professional Bookkeeping

A UK VAT bookkeeping benchmark has pushed GLM 5.2 to nearly the same level as human bookkeepers. Professional finance, long considered one of the hardest nuts for LLMs to crack, is now seeing open-source models tear open a breach.

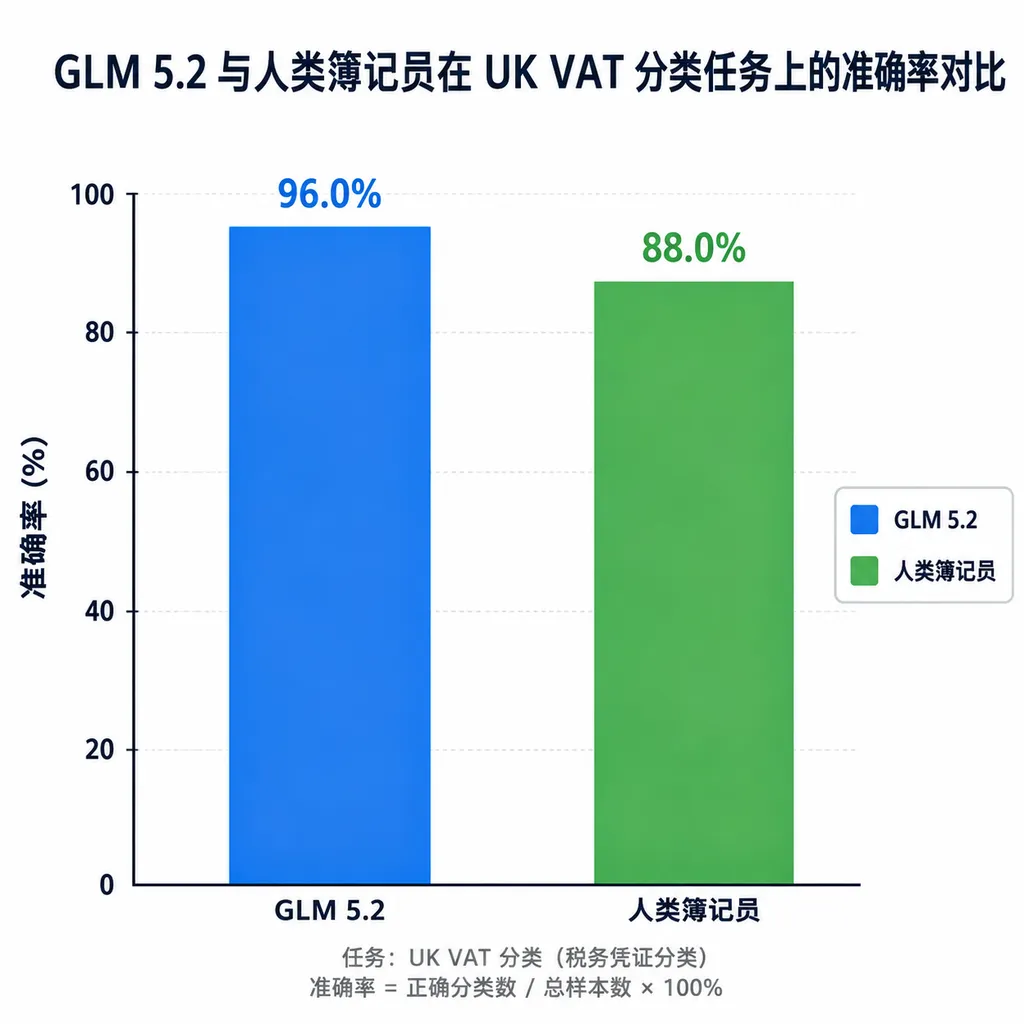

A fairly solid benchmark has come out of the UK: putting GLM 5.2 head-to-head with human bookkeepers in real VAT accounting scenarios. The result is unusual — the model’s accuracy is already running neck-and-neck with humans, and in some categories it even surpasses junior accountants. This is not just another leaderboard story. It’s the first time an LLM has been seriously evaluated inside a professional workflow where there are legal consequences, compliance red lines, and accountability for every mistake.

Until now, when people talked about the capability boundaries of LLMs, “professional finance” was usually placed on the protected side of the moat. Because bookkeeping is not like writing code — if code is wrong, maybe it fails to run and someone complains; if bookkeeping is wrong, you may need to refile VAT returns, pay penalties, or attract HMRC scrutiny. The significance of this benchmark is that it did not rely on toy problems. It used real company vouchers, real account mappings, and real UK VAT classification rules, measuring accuracy item by item.

What exactly did this benchmark test?

In simple terms, it fed the model a large batch of real invoices, bills, and bank transactions, then asked it to perform three tasks that bookkeepers handle every day:

- Account classification: Should this expense be categorized as “office supplies” or “business entertainment”? Put it in the wrong bucket and the quarterly tax filing becomes incorrect.

- VAT rate classification: Choose among Standard rate (20%), Reduced rate (5%), Zero-rated, Exempt, or Outside the scope. The boundaries are often subtle — for example, whether takeaway food is taxed at 20% or 0% depends on whether it is dine-in or takeaway, and whether it is hot food.

- Exception handling: Import reverse charge, partial exemption, place-of-supply determination for cross-border services — these are classic traps that routinely send junior bookkeepers back for retraining.

Human bookkeepers did not score 100% on this benchmark — real business operations never work that way. In the industry, experienced bookkeepers are generally considered strong at around 95% accuracy, while beginners are usually a bit above 80%. GLM 5.2 scored within the range of experienced bookkeepers and traded blows with top-tier closed-source models in the Opus 4.8 class.

More importantly, its performance on the hard problems stood out. The easiest VAT mistakes are the edge cases that “look like A but are actually B.” For example, whether an Uber receipt counts as commuting (non-deductible) or business travel (deductible) may depend on travel time, destination type, and even the role of the person initiating the trip. GLM 5.2 did not noticeably fall behind on these multi-field reasoning tasks, which aligns with its strengths in long-context and long-horizon task handling.

Why GLM 5.2 instead of something else?

To put it plainly, this result was not achieved through a single flashy trick. It came from stacking several capabilities together.

First, the long context window is genuinely usable. VAT bookkeeping is not a job where each voucher can be judged in isolation. How the same supplier was categorized last month, the company’s primary business, whether partial exemption adjustments were made, how prepaid expenses spanning multiple months are allocated — all of these are contextual factors. GLM 5.2’s stable 1M-token context window, combined with attention optimizations like IndexShare and HiSparse, allows it to bring the context of an entire ledger into scope at once instead of handling transactions one by one. Many models previously claimed million-token support but started losing information after 300k tokens. In bookkeeping, that is effectively laying a trap for yourself.

Second, stability in long-horizon tasks. Zhipu positions GLM 5.2 as a Long Horizon model capable of sustained eight-hour work sessions. This has already been repeatedly validated in software engineering scenarios — understanding entire repositories, tracking bugs across files, passing 38 backend tests in one run. Financial workflows are structurally very similar: not a single question-answer exchange, but a continuous process involving document intake, classification, reconciliation, tax return generation, anomaly detection, rollback, and review. Forget one step midway, and the final result becomes wrong.

Third, open source and compliance. This is what actually pushes it into real financial workflows. Accounting firms, corporate finance departments, and tax agencies are not going to upload client ledgers into an overseas closed-source API. GDPR, confidentiality agreements, and internal compliance requirements make that impossible. GLM 5.2 is open-sourced under the MIT license and can run on local machines or private clouds, keeping accounting data in-house. Right now, only the open-source ecosystem can offer that.

What does this actually mean for the finance industry?

First, some cold water: this does not mean bookkeepers will lose their jobs tomorrow. The benchmark’s failure cases make the limitations very clear. GLM 5.2 approaches human performance on classification tasks where rules are explicit and context is sufficient, but it still cannot handle situations that require calling clients for clarification, judging commercial substance, or communicating with tax authorities. Accounting has never been just typing at a keyboard.

But a large portion of the underlying operational work will inevitably be absorbed. The current industry workflow roughly looks like this:

- Voucher entry and initial classification: A junior bookkeeper processes dozens of entries per hour, consuming large amounts of time in small accounting firms.

- Reconciliation and anomaly detection: Bank reconciliation, supplier reconciliation, internal account reconciliation.

- Month-end closing and filing: VAT quarterly filings, CT600 corporate tax returns, Making Tax Digital submissions.

- Consulting and judgment: Advising clients on transaction treatment, tax planning, audit response.

Models in the GLM 5.2 class can already handle most of the first two layers. The third layer becomes semi-automated — generating drafts that accountants review. The fourth layer is unlikely to move anytime soon because it requires professional certification, human communication, and signed accountability.

What will really change is the cost structure of accounting firms. Previously, junior positions were mandatory. Now, one senior accountant paired with an AI workstation may be able to cover the workload that once required two or three junior staff. For small firms this becomes a survival issue; for large firms, a profitability issue.

From an engineering perspective: how to integrate GLM 5.2 into financial workflows

If you are building an AI-assisted bookkeeping system for clients or your own team, there are several things that need careful thought:

1. Never let the model post directly to the ledger. No matter how high the accuracy, LLM outputs should never write directly into the general ledger. The correct architecture is: the model generates suggestions, humans review them, and the system posts the entries. Audit traceability requires every record to be traceable back to “who approved what and when.” That responsibility cannot be delegated to AI.

2. Structured output is mandatory. Have the model produce JSON directly, with fields including suggested account, VAT classification, confidence score, referenced historical vouchers, and reasoning basis. Low-confidence items should automatically enter a human review queue. This workflow is far more practical than asking the model to “write an explanation.”

3. Context feeding must be carefully designed. Dumping the entire ledger into the context window is wasteful — not every model stays coherent beyond 800k tokens. A better approach is to include relevant historical vouchers for the current transaction (same supplier, same account category, last 90 days), the company’s bookkeeping policy manual, and VAT adjustment rules for the current filing period. There is no need to drag in irrelevant transactions from three years ago.

4. Edge cases require dedicated evaluation sets. Partial exemption, reverse charge, mixed-use assets, EU cross-border services, second-hand goods Margin Scheme — each category deserves its own regression test set. Whenever the model is upgraded, rerun the suite and check which categories regressed.

5. Do not overlook language. Many UK VAT rules are essentially text-based judgment problems, and the model’s understanding of English legal language directly affects performance. The same applies to Chinese VAT scenarios, where specialized terminology and local interpretations matter heavily.

The larger signal

Viewed narrowly, this benchmark says “GLM 5.2 performs well in UK bookkeeping.” Viewed more broadly, it shows that open-source models are expanding horizontally from their traditional stronghold in coding into professional vertical domains. Previously, GLM rose into the top tier of AI coding models through long-context and long-horizon agent capabilities; now those same strengths are proving effective in financial workflows. The next likely targets are legal documents, clinical records, audit working papers, and supply-chain document processing — all scenarios characterized by “context-heavy + long-horizon workflows + strict compliance boundaries.”

This creates a sharp contrast with recent developments around Anthropic. Not long ago, Fable 5 and Mythos 5 were required by the U.S. Department of Commerce to shut down global access, making “whether the model will still be usable tomorrow” a real concern for closed-source frontier models. Enterprise model selection now requires another evaluation column beyond performance: “Will it still exist tomorrow morning?” Open weights, local deployment, and an MIT license together make that column read “yes.”

So the real point of this news is this: the next valuation anchor for LLMs will not be “whose benchmark score improved by another 0.5 points,” but “who actually entered professional workflows and stayed there.” GLM 5.2’s performance on the UK bookkeeping benchmark is the first truly solid data point along that line.

Incidentally, platforms like OpenAI Hub allow a single API key to access GLM, Claude, and GPT series models simultaneously, which saves a lot of integration effort when running multi-model evaluations. But when it comes to production financial environments with sensitive data, locally deployed open-weight models are still the preferred route — those two use cases should not be confused.

References

- GLM-4.5 GitHub Repository — Public repository for the Zhipu GLM series, including the technical lineage and deployment examples for the GLM 5 family

- Z.AI GLM Models on Hugging Face — Official release page for GLM 5.2 open weights, model cards, and inference configurations

- Zhihu: GLM-5.2 Discussions — Chinese technical community discussions and evaluations of GLM 5.2’s long-context and long-horizon task capabilities

- Reddit r/LocalLLaMA — First-hand community feedback on local deployment and professional use cases for the GLM series in the open-source LLM ecosystem