OpenRouter Targeted by Tech Giants: The 1.3 Billion Valuation May Be Just the Beginning

OpenRouter, the world’s largest AI model aggregation platform, has reportedly been in acquisition talks with several tech giants, with its valuation expected to surpass $1.3 billion. Only two months after its Series B funding round, why is this “middleware” business so attractive?

The Information just dropped a story: OpenRouter has received acquisition offers from several tech giants, with bids possibly exceeding its $1.3 billion valuation from its Series B round two months ago. As of publication, OpenRouter has not responded, but the industry is already buzzing—who will be the buyer?

The significance here isn’t whether the deal closes, but that a company which neither trains models nor offers compute—only acts as an “API translation” layer—is being treated by major players as a strategic prize.

From $547 million to $1.3 billion in just 11 months

Let’s lay out the timeline so you can see how impatient capital has been with this company:

- June 2025: Series A, post-money valuation $547 million

- May 2026: Series B $113 million raised, led by CapitalG (Alphabet’s growth fund) with NVIDIA NVentures joining, a16z and Menlo Ventures increasing stakes; post-money valuation $1.3 billion

- July 2026: Multiple tech giants rumored interested in acquisition, bids above $1.3 billion

Its valuation doubled in 11 months, and two months later suitors are already lining up. That pace is rare in today’s AI scene—most star projects wait at least six months after fundraising before the next big story. OpenRouter moved straight into “being fought over.”

From the fundamentals, this valuation is justified but not cheap. Annualized revenue is about $50 million—implying a 26× P/S ratio. For comparison, The Information reported in Dec 2025 that AI application companies averaged ~53× forward revenue multiples—making OpenRouter a relatively conservative valuation. The reason is clear: its business is a channel business; commission-based margins are lower than pure SaaS. That 5–5.5% take rate looks attractive, but it must cover upstream token costs, bandwidth, infrastructure, and reliability maintenance.

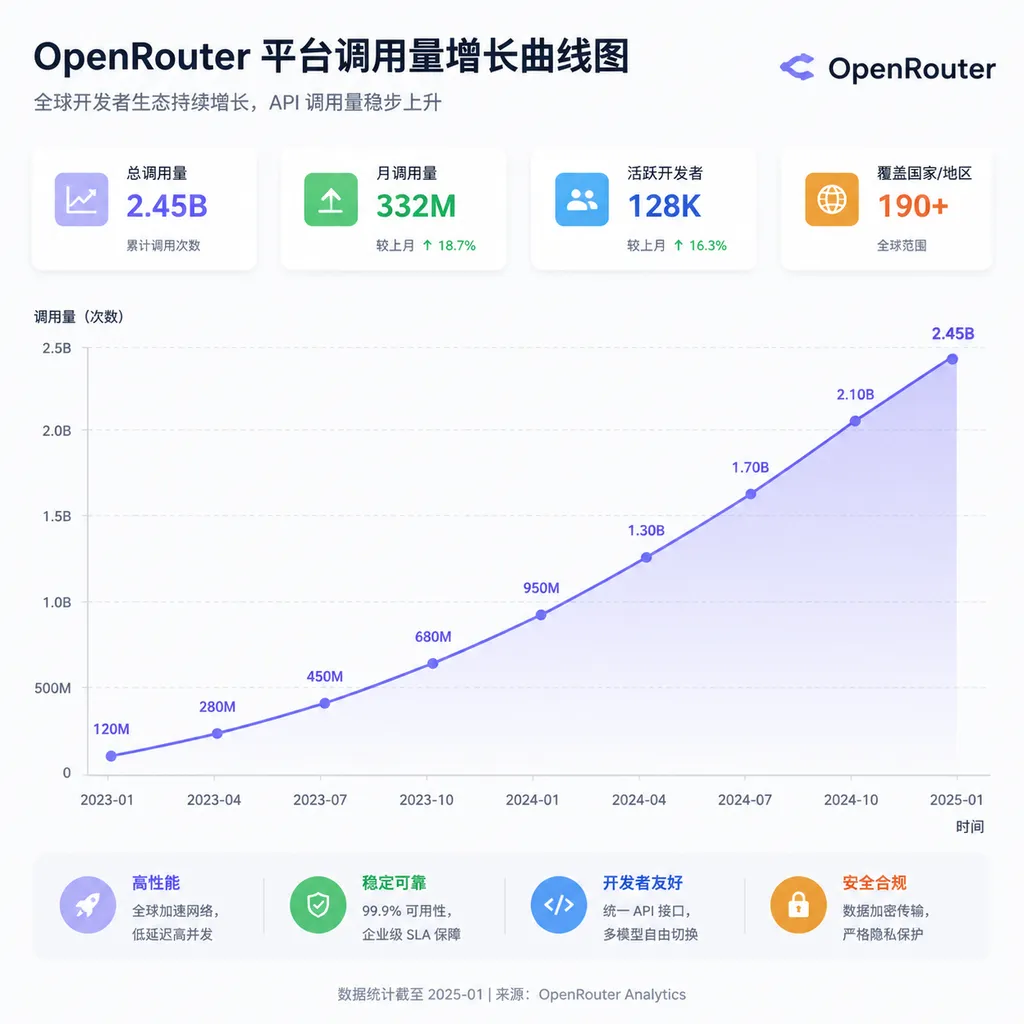

8 million users, 100 trillion tokens per month—what is it actually selling?

In one line: OpenRouter sells freedom from choosing models.

Over the past two years, mainstream models have mushroomed from a dozen to more than 400 —OpenAI, Anthropic, Google, DeepSeek, Moonshot AI, MiniMax, Zhipu, Step Fun… Each uses different API specs, billing, and stability. A developer who wants to use Claude in Cursor today, switch to GPT tomorrow, and try DeepSeek V4‑Flash the next day must rewrite integration code each time.

What OpenRouter does is “translate” all APIs into the OpenAI‑compatible format, then layer on smart scheduling: automatically routing to the best model by task type, cost, and performance, and falling back automatically if one is down. It takes roughly a 5% fee per call.

That logic supports some eye‑popping metrics:

- Aggregated models: 400 +

- Global users: 8 million +

- Monthly token throughput: ≈ 100 trillion

- Annualized revenue: ≈ $50 million (up 5× from $10 million last October)

Put differently, 100 trillion tokens per month at roughly $1 per million tokens equals around $1 billion of inference spending transacted yearly. That scale means OpenRouter is no longer just an API broker; it’s a reference point for pricing in the global AI‑inference market. Every update to its Trending chart represents developers voting with real money.

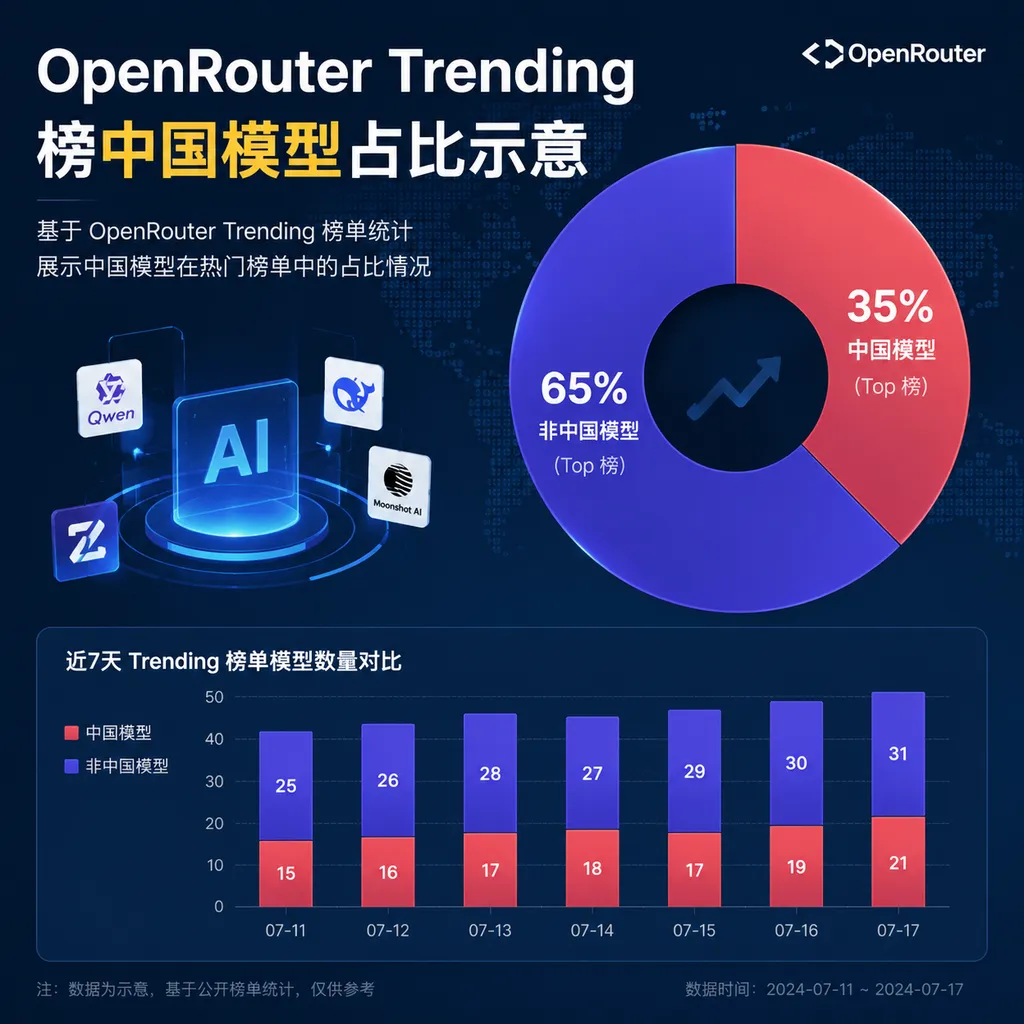

The rise of Chinese models behind the Trending chart—the hidden story of this acquisition

Treating OpenRouter merely as a commission platform underrates why giants want it. Its real strategic value is that it’s become the best window into global AI power shifts.

Some data:

- Early 2025: Anthropic 42.2%, Google 25.8% → combined ~68%; Chinese models < 15%

- Early 2026: Google 18.8%, Anthropic 14.7% → combined 33%; Moonshot AI 14.5%, DeepSeek 9.0%, MiniMax 4.2%, Qwen 2.6%; Chinese models ≈ 30%

- June 8–14 2026: Among 44.6 trillion tokens globally that week, the top four slots were all Chinese models—for seven straight weeks.

Within a year, Chinese models’ token share on OpenRouter rose 421%. DeepSeek‑V4‑Flash, MiniMax M3, Tencent Hy3 preview, Moonshot Kimi K2.5, Zhipu GLM‑5, Step Fun Step 3.5 Flash —all dominate the Trending list in rotation. Step 3.5 Flash hit #1 within two days of launch; MiniMax M2.5 became the #1 weekly model within a week.

For the giants, this means two things:

First, OpenRouter holds the most accurate “model market share report.” Closer to real developer choices than any research institute. Owning it means owning the data.

Second, it’s a natural distribution gateway. Coding‑related tokens jumped from 11% in early 2025 to 50% now—driven by Cursor and Claude Code explosions—making OpenRouter a core infra layer. Controlling the entrance outweighs controlling a single model.

Who’s buying? CapitalG is in; several others have motives

The Information didn’t name bidders, but the likely contenders with both motive and means are:

Alphabet/Google —most straightforward. CapitalG led Series B and likely has right of first refusal. Google needs a “neutral” distribution channel to counter Anthropic’s developer lock‑in via Claude Code; buying OpenRouter is a quick horizontal move.

Microsoft —its latest Office Copilot update hints at this: Copilot can now call OpenAI and Anthropic models simultaneously for cross‑checking. That multi‑model parallel architecture is almost identical to OpenRouter’s routing logic. Doing it in‑house is heavy; buying one off‑the‑shelf is simpler.

NVIDIA —already joined Series B via NVentures. Its usual strategy is “don’t bet on models, bet on inference demand.” OpenRouter perfectly aggregates that demand side.

AWS —can’t be ruled out. Its Bedrock service is a proprietary aggregator too, but lacks OpenRouter’s community buzz. The “buy vs build” debate has surely circulated inside Bezos’s team.

Curiously, OpenAI and Anthropic are the least likely buyers—their business models are precisely what OpenRouter “neutralizes.” Buying it would be an implicit admission that their models aren’t the only choice.

Why China can’t grow an OpenRouter

36Kr explained much of this earlier; here are a few deeper takeaways.

China does have similar players, grouped roughly as:

- Ecosystem types: Alibaba Cloud, Volcano Engine, Baidu Smart Cloud —aggregation as ecosystem extension

- Model developers’ open platforms: aggregation to retain developers

- Pure aggregators: SiliconFlow, ThinkFlow —closest to OpenRouter

- Overseas proxy types: resell GPT, Claude APIs to domestic devs—mostly gray areas

Why is a “Chinese OpenRouter” so hard?

Upstream is occupied by ecosystem players. Alibaba Cloud and Volcano Engine bundle models, compute, and dev tools—no room for pure middleware.

Downstream demand is about “compliance,” not “fragmented APIs.” High‑paying clients like finance and government care more about data security than API‑switching ease.

Gray‑area routes won’t last. Reselling ChatGPT Plus accounts as APIs or flipping free cloud credit might get rich overnight but invites regulatory risks. How non‑record‑filed foreign models could enter China’s AI service filing system remains unclear and unprecedented.

In essence, OpenRouter thrived because OpenAI and Anthropic chose not to build their own developer ecosystems. Chinese giants like ByteDance and Alibaba are far more integrated —model‑to‑platform‑to‑application as one chain—leaving no “middle‑layer” space.

Some sober reflections

OpenRouter’s moat isn’t as deep as its valuation. It controls traffic entry but owns neither models nor compute. If an upstream vendor cuts access or raises prices, margins reshuffle. This is why its founders are moving into open‑source model integration and enterprise workflow tools—the ceiling for a pure gateway business is visible.

The “being acquired” signal itself is telling. A company two months post‑Series B already in M&A talks implies it may doubt independent growth. Middleware businesses are easily squeezed from both ends; aligning with a giant may be most rational.

For developers, one reliable entry matters more than many entries. Who owns OpenRouter may barely affect day‑to‑day users—aside from routing logic, pricing, and data ownership changes. What matters is: if you need a single key to access GPT, Claude, Gemini, and DeepSeek without account‑pool risk, the value of a compliant aggregator remains. Domestic services like OpenAI Hub, direct‑connect and OpenAI‑compatible API aggregators, are filling that gap.

The acquisition shoes haven’t dropped; OpenRouter hasn’t responded. But one thing is certain: the AI‑middleware spot is getting crowded.

References

- Report: World’s largest AI aggregation platform OpenRouter receives acquisition offers from multiple tech giants, valuation may exceed $1.3 billion — ITHome’s original coverage of the rumor

- Top‑tier AI hub raises $770 million, NVIDIA joins round — Zhihu column’s detailed breakdown of OpenRouter’s Series B funding, investors, and business metrics