Stripe enters the AI wallet game — agents can finally spend money on their own.

Stripe has officially launched the Link digital wallet for AI agents, allowing users to authorize AI agents to independently complete payments. This marks the first step at the payment infrastructure level toward paving the way for the Agent economy, signifying AI’s transition from “able to chat” to “able to transact.”

Stripe Enters the AI Wallet Arena: Agents Can Finally Spend Money on Their Own

Payment giant Stripe officially launched AI agent payment capabilities for its Link digital wallet today (April 30). Simply put: your AI agent can now make online payments autonomously—like a human swiping a card—once you’ve granted permission.

This isn’t a proof of concept, nor a line on a roadmap—it’s a real, integrated product that’s already online.

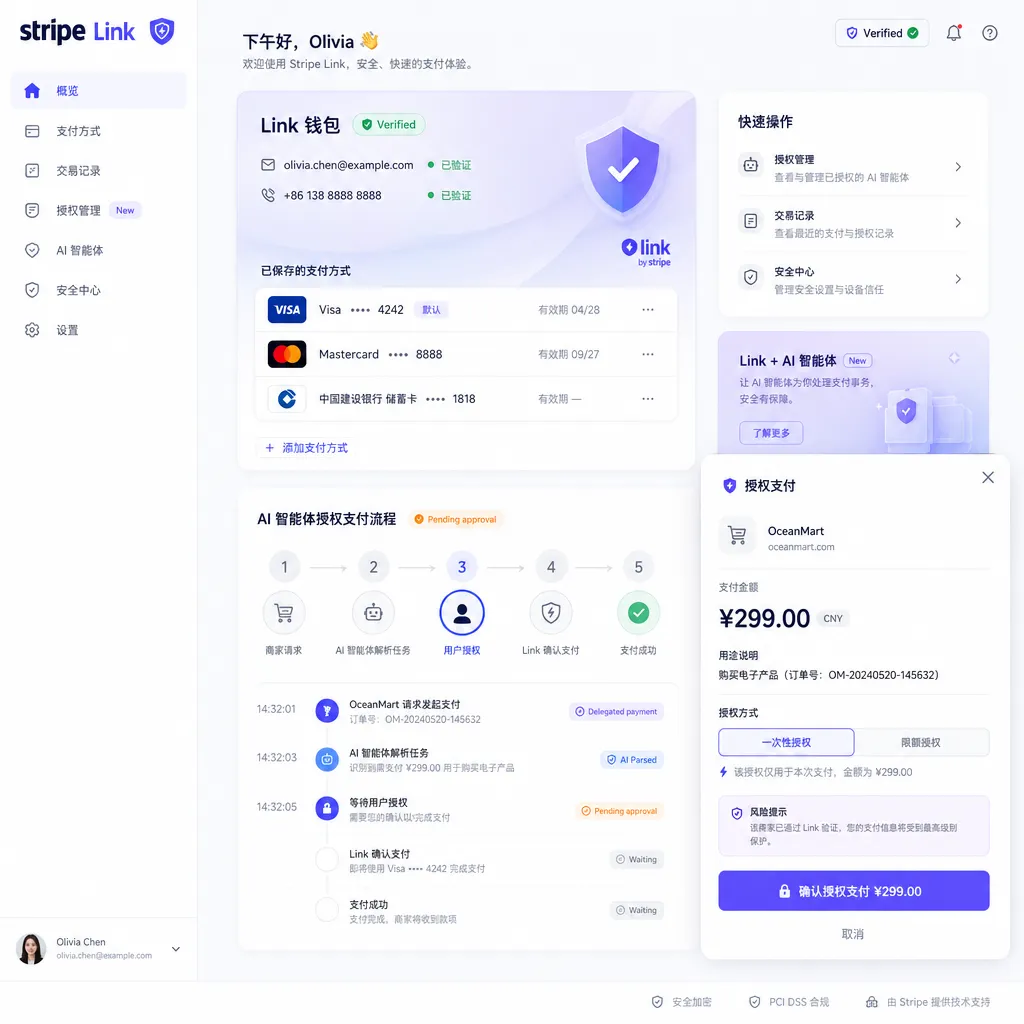

First, What Exactly Is Link?

Link isn’t an entirely new product. It started out as Stripe’s one-click payment tool—users could bind their bank cards or accounts to Link, and then, at any merchant that supports Stripe checkout, Link would automatically fill in payment details, saving users from retyping card numbers. You can think of it as a Stripe version of “Remember my payment method,” but implemented as a cross-merchant, cross-device universal layer.

The major upgrade this time: Link now serves not only human users, but also AI agents.

Specifically, users can:

- Bind credit cards, debit cards, or bank accounts

- Manage subscriptions and recurring payments

- Authorize specific AI agents to make payments on their behalf

- Set spending limits, approval flows, and scope of use for agents

Those last two points are crucial. Stripe isn’t just tossing an API key to an AI agent and letting it spend freely—it has built a complete authorization and approval system.

Authorization Mechanism: Delegation Without Losing Control

Anyone who works in payments knows that “who can spend money” is ten times harder than “how to spend it.” Stripe’s design here deserves a closer look.

Link’s AI agent authorization uses a layered approval model:

Layer 1: Explicit User Authorization. The user must actively enable agent payments in Link and specify which agents can use them. Permissions are not granted by default—it’s a whitelist system.

Layer 2: Spending Rules. Users can define single transaction limits, daily/monthly caps, and merchant category restrictions for each agent (for example, only allow SaaS purchases, not physical goods). It’s similar to how companies issue virtual corporate cards—spending is allowed, but only within set boundaries.

Layer 3: Real-time Approval Flow. For transactions exceeding preset rules, Link triggers an approval notification so the user can approve or reject with one tap. Agents can’t override limits just because they “think it’s necessary.”

The logic here is clear: AI agents are executors, not decision-makers. They act autonomously within the bounds you define, and must request approval beyond that scope.

Compare this with other existing agent payment approaches, most of which simply hard-code an API key into the agent so it can call payment APIs directly. The problem is obvious—no granular permission control. If an agent receives malicious prompts or hallucinates, the consequences could be disastrous. Stripe uses Link to separate payment credentials from agent logic—agents never hold actual payment information but only a restricted authorization token.

Why Now?

The timing makes perfect sense.

Over the past year, AI agents have moved from labs into production much faster than expected. OpenAI’s GPT series, Anthropic’s Claude, and Google’s Gemini have all been strengthening their agent capabilities—not just conversation, but autonomous actions like browsing, API calling, and performing multi-step tasks.

But every agent developer has hit the same wall: agents can help you research information, write code, send emails—but when actual payment is required, they get stuck.

A few real-world examples:

- You ask an agent to book a flight from Beijing to Shanghai—it finds flights, compares prices, but you still have to make payment yourself.

- You ask an agent to purchase cloud servers—it calculates configurations, selects regions, but the final payment step still requires human intervention.

- You ask an agent to manage SaaS subscriptions—it can analyze which to renew or cancel, but you must rejoin to execute transactions.

Each time “the human is pulled back into the loop,” it breaks the autonomy of the agent. Payment is the missing final piece of the agent’s operational cycle.

Stripe clearly noticed this. As one of the world’s largest online payment infrastructure providers (valued at $159B), its merchant coverage is massive. Link’s AI payment capability means, in theory, any merchant that supports Stripe can now accept agent payments—with no extra integration required on their side.

That network effect is hard for competitors to match.

Technical Implementation: What It Means for Developers

From a developer’s perspective, Stripe’s approach simply extends its existing API system to support agents—it doesn’t reinvent the wheel.

The Link agent payment flow looks like this:

- User creates agent authorization in Link, generating a restricted session token.

- Developer integrates Stripe SDK into the agent code, using that token to initiate payment requests.

- Stripe backend verifies token permissions, checking whether the transaction is within authorized limits.

- If valid, payment proceeds; if beyond limits, user approval is triggered.

- After completion, the agent receives a callback and continues its workflow.

Throughout the process, the agent never accesses raw payment credentials (card numbers, CVV, etc.). It only knows “I’m authorized to spend within a certain scope,” while Link handles the sensitive data server-side. This is crucial for security—even if an agent is compromised, attackers gain nothing useful from the payment data.

As a Level 1 PCI-certified provider, Stripe already leads the industry in encryption and compliance. Extending that capability to agents is much safer than having every individual agent developer try to handle payments securely on their own.

For developers already using Stripe, integration costs are minimal. Link’s agent payment feature is built as an extension of the existing Stripe Payment Intents API—no migration to new endpoints required.

The Bigger Picture: The Infrastructure Race for the Agent Economy

Stripe’s move into agent wallets takes on new meaning when viewed against the broader backdrop.

We’re witnessing the birth of a new economic paradigm: the Agent Economy. In this economy, AI agents are not just tools—they become participants in economic activity, capable of purchasing, consuming, and transacting on behalf of humans (or even companies).

This isn’t science fiction. Look at what’s happening right now:

- Tempo, a project focused on AI agent payments, launched its mainnet this month with a “machine payment protocol,” and hosted the first AI payment hackathon in San Francisco.

- Klarna has integrated its “buy now pay later” (BNPL) service with Stripe Link, meaning agents can even make installment payments.

- Several Web3 projects are experimenting with stablecoins as settlement media between agents.

Stripe’s entry instantly raises the baseline infrastructure level of the entire field.

Up until now, most players in this space have been startups building from zero to one. Stripe is different—it brings:

- An existing merchant network: millions of merchants worldwide already use Stripe, so agents can transact immediately.

- A mature risk control system: Stripe Radar’s anti-fraud tools can directly apply to agent transactions.

- Compliance frameworks: PCI DSS, PSD2, SCA, and other regulatory standards are already handled by Stripe.

- Developer ecosystem: Stripe SDKs cover all major languages, with documentation standards that are industry-leading.

In short, Stripe isn’t just shipping a product—it’s upgrading the entire payment infrastructure for the agent era.

Concerns and Challenges

Of course, it’s not all smooth sailing.

Trust is the biggest hurdle. Allowing an AI to spend money on your behalf is a significant psychological leap for most users. Even with all security controls in place, trust takes time to build. Remember how few people were comfortable linking their bank cards to mobile payment apps at first? The trust-building process for agent payments will likely take even longer.

Liability remains a gray area. If an agent makes a purchase within its authorization but you didn’t actually want it (e.g., it “decides” to renew a subscription you meant to cancel), who’s responsible? A user might claim, “I didn’t tell it to buy that,” merchants might say, “The transaction was properly authorized,” and developers might insist, “The agent followed its logic.” Current consumer protection laws don’t yet cover such cases.

Agent judgment isn’t fully reliable. Today’s large language models still hallucinate, and any hallucination involving money could have real consequences. Stripe’s layered approval helps mitigate this, but if a user’s limits are too loose (say, automatic approval for transactions under $500), the agent can still make costly mistakes within that range.

Regulation hasn’t caught up. Globally there’s no clear regulatory framework for agent payments. Is an agent considered a “payment proxy”? Does it require separate KYC? If it makes cross-border purchases, which country’s laws apply? The answers are unclear. As a compliance leader, Stripe will likely take an active role in regulatory discussions—but that will take time.

Industry Impact

In the short term, Stripe Link’s agent payment feature will accelerate a few key trends:

1. Commercialization of Agent-as-a-Service. Many agent products have struggled with monetization—agents can help users get things done but couldn’t directly complete transactions. Now, with the payment loop closed, agents can truly become “assistants that spend for you,” and developers can monetize through transaction fees.

2. Enterprise Agent Procurement. Scenarios such as agents automatically purchasing office supplies, renewing SaaS tools, or managing cloud resources will likely be early adopters—enterprise usage has clearer spending rules, established approval processes, and more controllable risk.

3. The Payment Industry’s Agent Adaptation Race. With Stripe’s move, PayPal, Adyen, and Square won’t just sit idle. Expect major payment platforms to roll out similar agent payment capabilities within the next six months.

In the long run, the implications could be far greater than we imagine. If agents truly become regular participants in economic activity, payment infrastructure will evolve from a “human-to-merchant” pipeline to a “human-to-agent-to-merchant” or even “agent-to-agent” network. That would reshape the architecture of the entire payment industry.

Stripe is clearly betting on that future—and a $159B company doesn’t make noise for a small feature.

Final Thoughts

Returning to the most practical question: Can you use this now?

Yes. Link’s agent payment capability is live, and developers can start integrating via Stripe’s official documentation. For teams already on Stripe, migration is minimal; for newcomers, Stripe’s SDKs and documentation remain top-tier.

But “usable” isn’t the same as “frictionless.” Agent payments represent an entirely new interaction paradigm—user habits need to form, edge cases need refinement, and regulatory frameworks need development. Stripe has taken the first crucial step, but this path will be a long one.

One thing’s certain though: the shift from “agents that talk” to “agents that spend and earn” has already begun—and Stripe is positioning itself as the infrastructure beneath that transformation.

This article focuses on payment product updates, not a newly released closed-source model, and does not include API call code samples.

References

Note: Only sources accessible within China are retained. Other information is based on Stripe’s official announcement and TechCrunch reports.

Since main sources (TechCrunch, Stripe official site, Binance, etc.) are hosted on overseas domains not accessible domestically, no direct links are provided. Readers can search “Stripe Link AI Agent Payment” for more related coverage.