NVIDIA teams up with LG to build an AI factory, Isaac + GR00T to create a Korean robot base

NVIDIA and LG Group announce joint construction of an AI factory in Korea, integrating full-stack platforms such as Isaac Sim and GR00T, covering CLoiD training for household robots, physical AI data production, ADAS development, and EXAONE model iteration powered by Blackwell, aiming to set a global benchmark for intelligent manufacturing.

Nvidia Teams Up with LG to Build AI Factory, Isaac + GR00T to Create Korea’s Robotics Base

Nvidia just painted a grand vision for the global robotics ecosystem at GTC, and immediately turned around to finalize an implementation plan with the LG Group. The AI factory announced on June 8 is not a simple computing power stack, but rather a packaged integration of Isaac simulation, the GR00T foundation model, the Cosmos world model, Blackwell GPU, and the DSX data center platform—directly embedded across LG’s entire business line, from household robots to industrial production lines, from ADAS to the self-developed EXAONE large model.

The signal from this cooperation is clear: Nvidia wants to run its closed-loop "physical AI" toolchain—from simulation to deployment—through Korea's manufacturing system, proving that an end-to-end AI factory is more than just a PPT concept. LG, for its part, needs Nvidia’s infrastructure to quickly shore up weaknesses in robotics and autonomous driving, while providing its EXAONE large model with stronger computing and data support.

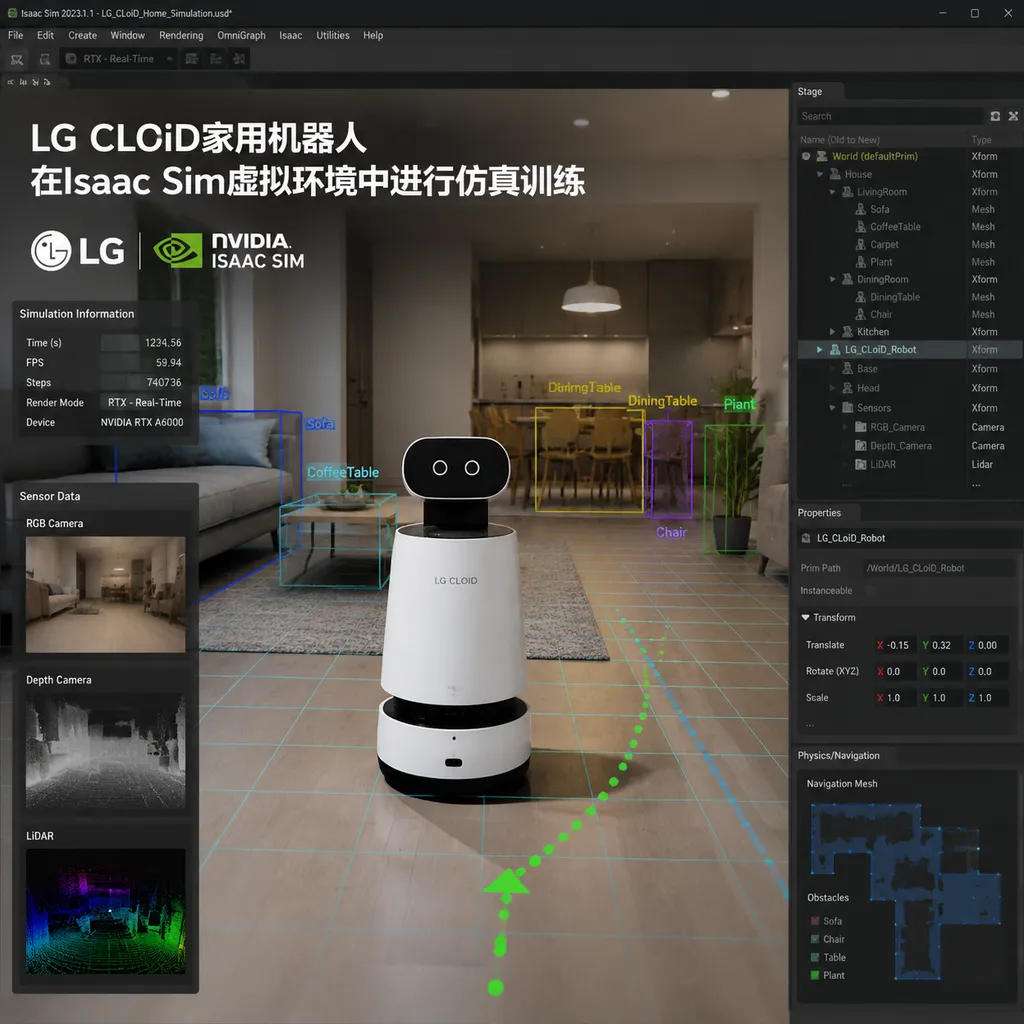

Household Robot CLoiD: the “Digital Nanny” Trained in Isaac Lab

LG Electronics’ CLoiD household robot is positioned as an indoor assistant capable of doing chores and understanding voice interaction. But household environments are far more complex than industrial production lines—irregular room layouts, randomly placed objects, and unpredictable human behavior all require robots with strong generalization ability. The traditional approach—collecting huge amounts of real-world data for training—comes with high cost, long cycles, and an overfitting risk to specific scenarios.

Nvidia’s solution is the Isaac Sim + Isaac Lab + GR00T trio. Isaac Sim provides physically accurate virtual environments, capable of simulating lighting, materials, collisions, and other real-world features; Isaac Lab 3.0 (based on Newton Physics Engine 1.0) enhances multi-physics simulation and dexterous manipulation, enabling robots to learn fine-grained actions in a virtual space—such as grasping fragile objects, opening doors, folding clothes; the GR00T N1.7 model offers vision-language-action reasoning, enabling the robot to understand vague commands like “tidy up the living room” and break them down into executable action sequences.

The core advantage of this combination is synthetic data generation capability. LG’s in-construction “physical AI data factory” plans to use the Cosmos world model to generate training data at scale, and then verify policy effectiveness in Isaac Lab. Cosmos, Nvidia’s newly released world foundation model, can generate physically realistic 3D scenes and action sequences from textual descriptions. For example, input “robot pouring water in the kitchen” and Cosmos can produce thousands of variant scenes with different kitchen layouts, cup materials, and pouring angles. These datasets are then used in Isaac Lab to train policy networks.

This data factory will serve not only LG itself. Official statements say LG will open this capability to robot companies in Korea and worldwide—in essence, aiming to be a “data supplier” in the physical AI era. Considering Isaac’s ecosystem already includes humanoid robotics players such as 1X, Zhiyuan Robotics, Agility, and Figure, if LG can ensure high data quality, the business growth potential here is considerable.

However, a practical problem exists: while the GR00T model is open-source, getting it to run optimally in specific products requires heavy domain data fine-tuning and hardware adaptation. LG and Nvidia plan to jointly develop a “reference model”—essentially customizing and tuning GR00T to fit CLoiD’s hardware and task requirements. How fast this process runs and whether performance can outcompete rivals (such as Figure’s use of OpenAI’s multimodal model) will directly determine CLoiD’s market competitiveness.

Industrial Robots: Bringing FANUC’s Virtual Commissioning to the Isaac Platform

LG CNS (LG’s IT services subsidiary) plans to integrate Nvidia’s robotics technology into its PhysicalWorks industrial platform—an even more direct play at capturing AI upgrade dividends in industrial automation.

PhysicalWorks itself is LG CNS’s digital twin + MES (manufacturing execution system) solution for manufacturing, serving primarily LG’s own factories and some Korean industrial clients. Adding Isaac simulation capabilities means these factories can complete production line design, robot programming, collision detection, and cycle optimization in a virtual environment, then deploy to physical lines in one click.

Another notable GTC announcement: FANUC, ABB, YASKAWA, and KUKA—together controlling over 70% of the world’s industrial robot installs—are integrating Isaac’s simulation framework into their virtual commissioning tools and plan to embed Jetson modules in controllers for edge AI inference. This means future factory-floor robots could train new skills in the cloud with Isaac Lab while performing real-time edge-side tasks like vision recognition and path planning.

LG CNS’s bet here is essentially to secure a position on the “AI factory as a service” track. Traditional industrial automation is a one-off sale of hardware + software licenses; but if simulation, training, deployment, and O&M become cloud subscription services, customer stickiness and profit margins climb. The problem is that incumbents like Siemens and Rockwell are pursuing similar strategies, and LG CNS’s differentiation remains limited.

Autonomous Driving: Aligning with DRIVE Hyperion, But Not as a Tier 1

LG Electronics aims to align with Nvidia’s DRIVE Hyperion architecture to advance its ADAS and software-defined vehicle (SDV) product lines. It’s important to note here: LG is not positioning itself as a Bosch- or Continental-type Tier 1 supplier, but as a combination supplier of in-vehicle components + in-vehicle OS.

DRIVE Hyperion is Nvidia’s reference architecture for L2+ to L4 autonomous driving, comprising sensor configurations (cameras, lidar, millimeter-wave radar), compute platforms (DRIVE Orin/Thor chips), and software stacks (perception, planning, control algorithms). LG Innotek (LG Electronics’ optics module unit) plans to offer sensor solutions customized for DRIVE, directly competing with Sony and Samsung Electro-Mechanics.

More crucially, LG Electronics has its own in-vehicle OS and domain controllers. Over the past few years, LG has been negotiating pre-install partnerships for webOS Auto (based on open-source webOS) with GM and Stellantis. If DRIVE’s autonomous driving capabilities can be integrated, LG could offer automakers an “OS + ADAS” bundled solution. This mirrors Huawei’s MDC (Mobile Data Center) approach—bypassing traditional Tier 1 to plug directly into the intelligent driving soft/hardware integration tier.

However, LG faces the issue of lacking both Tesla’s closed-loop driving data (from millions of vehicles in real-world operation) and Waymo/Cruise’s Robotaxi road-testing experience. ADAS algorithm maturity is therefore questionable. Aligning with DRIVE Hyperion provides Nvidia’s toolchain and ecosystem endorsement, but true competitiveness depends on LG securing enough mass-production projects and accumulating sufficient corner case data.

AI Factory Infrastructure: Blackwell + DSX + 800V DC Storage

LG Uplus (telecom operator) and LG CNS will build “scalable AI factories” based on the DSX platform; LG Energy Solution is exploring 800V DC data center energy storage. Viewed together, they reveal LG’s ambition in AI infrastructure.

DSX (Data Center Scale Experience) is Nvidia’s reference architecture for enterprise AI deployment. It packages DGX servers, InfiniBand network, storage, and cooling solutions into standardized modules so enterprises can rapidly build AI training/inference clusters. LG Uplus already operates data centers; now with DSX, it aims to offer AI compute as a cloud service to enterprise clients—following the same logic as AWS, Azure, and Alibaba Cloud.

LG Energy Solution (the battery arm) is targeting the energy consumption pain points of AI data centers with 800V DC storage. Blackwell GPUs draw over a kilowatt each; training clusters can run into tens of megawatts. Traditional AC power distribution has high loss and slow response. An 800V DC approach reduces AC-DC conversion stages, boosts efficiency, and uses batteries for peak-shaving to cut costs. Tesla’s Dojo supercomputer center and Meta’s AI Research Supercluster use similar setups. If LG Energy Solution can carry over its automotive battery cost and safety advantages into data center applications, growth potential here is significant.

However, timing poses a challenge. Blackwell GPUs only begin large-scale shipment this year, and the DSX ecosystem is still in its early stages; large-scale AI factories may not be fully operational until 2027. LG’s ability to harmonize hardware, software, and O&M systems over that period will determine how much of the AI infrastructure market it can capture.

EXAONE Large Model: Asking Blackwell for More Tokens

LG AI Research Institute is continuously developing the EXAONE model on Blackwell GPUs and promoting it internally via ChatEXAONE. EXAONE is LG’s self-developed multimodal large model; the 3.0 version released last year has about 70B parameters—still trailing GPT-4 and Claude 3 in benchmarks—but features targeted optimizations for Korean language processing and enterprise tasks (e.g., contract analysis, customer service dialogues).

Blackwell GPUs offer 4× training throughput and 25× lower inference cost compared to the previous Hopper generation (per Nvidia). For EXAONE, that means training larger-scale models or extending pretraining with more data at the same budget. LG’s strategy is clear: avoid competing with OpenAI and Anthropic on general-purpose capabilities, instead building an “industry LLM for Korean enterprises” focusing on manufacturing, retail, finance, and telecom.

ChatEXAONE, akin to Microsoft’s Copilot, is already in trials at LG Electronics, LG Chem, LG CNS, and other subsidiaries. Yet externally, EXAONE’s commercialization appears slow: few public customer cases and no obvious superiority over closed models like Claude, GPT-4o, and Gemini. Whether Blackwell’s compute boost can push EXAONE from “usable” to “truly good” will require at least six months of validation.

The Real Focus of This Partnership: Can an End-to-End AI Factory Run?

Nvidia’s “AI factory” concept—promoted over the past year—hinges on turning data generation (Cosmos), simulation training (Isaac Lab), model deployment (Jetson/DRIVE), and inference optimization (TensorRT) into an end-to-end standardized pipeline, sparing enterprises the need to build AI infrastructure from scratch. Yet real-world proofs remain few.

LG’s role here is essentially to give Nvidia a “full-stack stress test.” From dexterous handling in household robots, to industrial-line digital twins, to sensor fusion in autonomous driving, to continual training of large models—every link will use different modules of Nvidia’s AI factory. If all these business lines land as planned, Nvidia’s end-to-end toolchain will be validated; if one link jams, the bottlenecks in Isaac/GR00T/Cosmos will be exposed.

For LG, the risk is technical lock-in. Once deeply bound to Nvidia’s hardware and software stack, shifting later to another vendor (e.g., AMD MI300 or Intel Gaudi) becomes difficult. But given Nvidia’s lead in AI hardware and ecosystem, LG has few short-term alternatives. The more immediate question: can LG truly translate Nvidia’s general-purpose toolchain into its own product competitiveness—can CLoiD understand user needs better than rivals, can PhysicalWorks outperform Siemens, can EXAONE meet Korean corporate compliance needs better than GPT? Answers will likely only emerge when this batch of AI factories enters production around 2027.

This Nvidia–LG partnership is not simply “selling cards + providing tech support”; it’s a bet on a larger question: In the physical AI era, can a closed-loop toolchain from simulation to deployment become the next cloud-computing-scale platform business? If the bet pays off, Nvidia becomes more than a GPU vendor—it becomes an AI infrastructure platform provider. If not, the investments in Isaac, GR00T, and Cosmos may amount only to a few open-source frameworks for the developer community.

For LG Group, this big bet makes it both a validator and a beneficiary. For a Korean conglomerate with $180B in annual revenue spanning consumer electronics to chemical materials, AI transformation is a must, not an option. Choosing Nvidia as a partner at least minimizes technical missteps. But whether LG can truly convert the compute advantages of AI factories into market product advantages will depend on its own product definition capability and execution efficiency.

Sources

- Nvidia and LG Group Join Forces to Build AI Factory, Advancing Physical AI and Mobility – IT Home — Official cooperation details and business scope

- NVIDIA Teams Up with Global Robotics Leaders to Bring Physical AI into the Real World – NVIDIA Official Blog — Isaac ecosystem partners and technical framework overview