Ant International launches AMP protocol, providing a standard solution for agent-based cross-border payments

Ant International has officially released the Mobile Agent Protocol (AMP), providing a standardized solution for global AI agent-based shopping and cross-border payments, addressing three major pain points: payment convenience, security, and merchant connectivity.

Ant International Launches AMP Protocol, Providing a Standard Solution for Agentic Cross-Border Payments

Ant International has recently officially released the Agentic Mobile Protocol (AMP), the world’s first protocol standard specifically designed for AI agent cross-border payment scenarios. The timing is noteworthy — just one week after Alipay’s high-profile launch of the AI Wallet at the end of May and completion of 300 million agent-based payment transactions, Ant’s overseas business line moved this payment approach into the global market.

The Cross-Border Dilemma of Agentic Payments

In China, the basic model for agentic commerce is already established. Alipay AI Pay supports 95% of general AI agent frameworks, and large model providers such as MiniMax and Step Star have integrated into it, connecting the full chain of token top-ups, membership subscriptions, and marketing. But going global is a different matter.

Cross-border scenarios are an order of magnitude more complex than domestic cases. First, payment methods are highly fragmented — the Asia-Pacific region has 40 different e-wallets and QR code networks across 11 countries, with vastly different consumer habits in each market. Koreans use Naver Pay, Thais use PromptPay, Malaysians use Touch 'n Go — how is an AI agent supposed to choose?

Second, the settlement and clearing process is long. Agents must help users place orders, pay, and process refunds in different markets, involving multiple currency exchanges, cross-border fund transfers, and local regulatory compliance. If any step fails, the entire transaction collapses.

The most critical issue is trust. Users delegate purchasing decisions to AI; if an agent is attacked, the payment instructions are tampered with, or the transaction record cannot be traced, who will take responsibility? Domestically, Alipay’s credit guarantees trust, but in overseas markets, why should merchants and consumers believe you?

The AMP protocol is designed specifically to address these pain points.

What AMP Protocol Solves

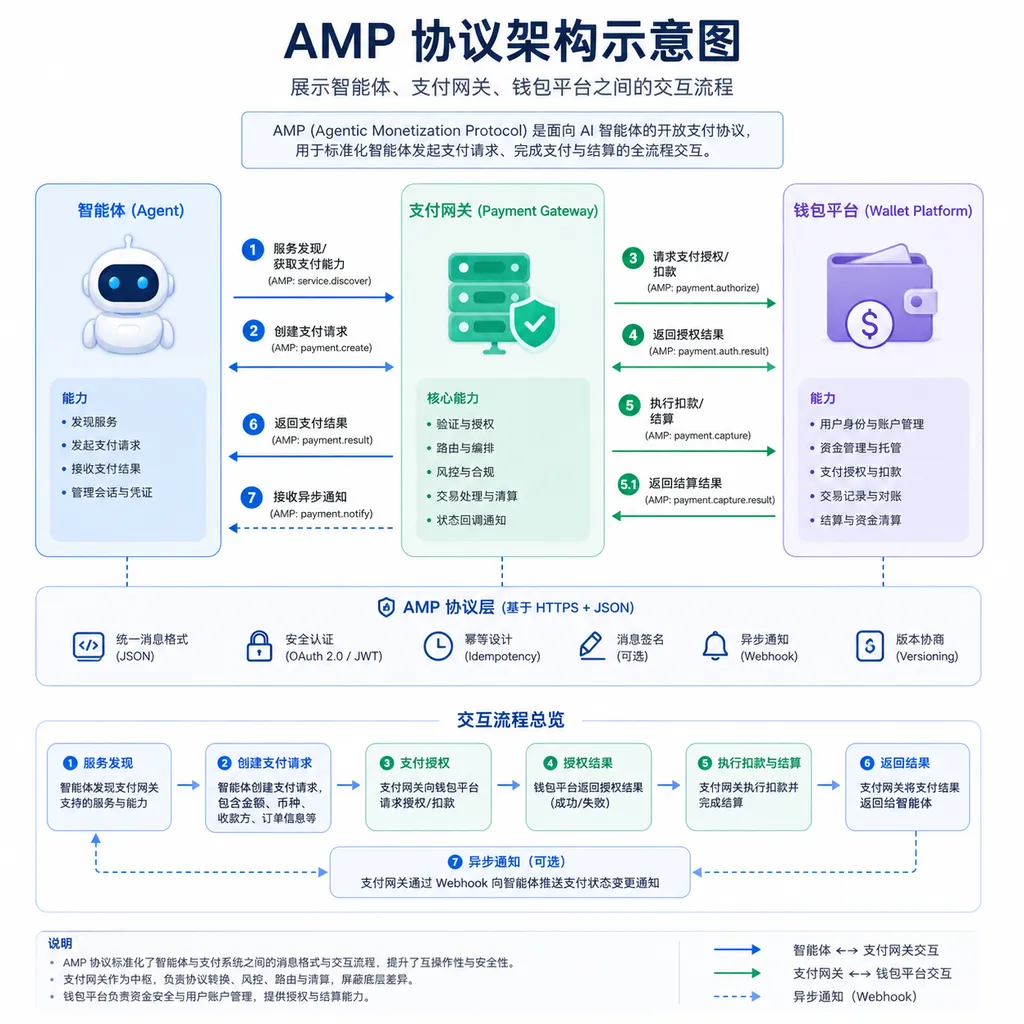

From a technical architecture standpoint, AMP does three things:

First, unified payment interface. At the protocol level, it abstracts a standardized payment instruction model so that agents only need to call a single API to connect to hundreds of payment methods worldwide. Ant International’s Antom service aggregates over 300 payment methods covering more than 200 markets; AMP packages this capability into agent-friendly interfaces.

This design is clever. Agent developers don’t need to study each market’s payment ecosystem or write adaptation code for different wallets. Whether your agent buys coffee for users in Thailand, books concert tickets in Korea, or tops up mobile credit in Malaysia, it all calls the same protocol in the background — Antom routes to the correct payment channel.

Second, trusted authorization mechanism. AMP uses the Model Context Protocol (MCP) to implement conversational payments and introduces AI user intent analysis and authorization models. In simple terms: before an agent initiates payment, the system associates key transaction parameters (amount, product, recipient) with the user’s dialogue context to generate a verifiable credential.

This credential is similar to a blockchain hash but implemented through multi-party computation (MPC) privacy computing. The benefit is that it can prove “this transaction was truly authorized by the user” without exposing chat records or payment details. In case of disputes, the credential query mechanism allows tracing to see if the AI’s understanding of the intent was correct.

Third, multi-layer security protection. Antom’s AI risk control system adds agent-specific safeguards on top of PCI security standards: mobile device security, identity hijacking detection, and transaction fraud recognition. Specific measures include multi-modal biometric authentication (iris + voiceprint, i.e., Alipay + GlassPay), real-time risk scoring, and interception of abnormal behaviors.

Ant International is also piloting credit card agent payments with Mastercard and Visa. Traditional credit card transactions rely on CVV, 3D verification, and other human interaction steps, which don’t work in agent scenarios. They are replacing plaintext card numbers with tokenization — agents get a one-time token rather than the actual payment credential, and even if the token leaks, it cannot be reused.

Key to Commercialization

The protocol itself is not valuable — the key is who uses it and how.

AMP’s target customers are global e-wallets, super apps, and digital banks. Ant International has already partnered with 40 e-wallets in Asia-Pacific; now, the goal is to persuade these wallets to integrate AMP so their users can complete cross-border purchases via AI agents.

For wallet platforms, the incentive to adopt AMP is: (1) lower integration costs — no need to develop payment plugins for each AI application; (2) expand usage scenarios — as the agent economy grows, payment frequency and transaction size will increase; (3) data feedback — analyzing agent transaction behavior to better understand user needs and improve product experience.

Ant International’s reported figures: by 2025, Alipay+ services will cover more than 100 markets, connect over 150 million merchants and 1.8 billion consumer accounts, and cross-border payment service WorldFirst will process nearly $200 billion in transactions — with year-on-year growth close to 100%. This scale means that if AMP spreads, it can instantly tap into a massive commercial network.

Merchant pain points are even more direct. For industries such as cross-border e-commerce, travel, and digital content, users are scattered worldwide and payment methods are diverse. Previously, merchants had to connect with a dozen payment service providers, each with different technical documentation, settlement cycles, and rates — leading to high operational costs. If AMP can standardize this process, merchants can integrate once to cover the global market, which is highly attractive.

Ant International’s Antom has already open-sourced an agent payment solution on GitHub. This move is similar to OpenAI’s API opening — let developers enjoy the benefits, run typical scenarios, and then push wallets and merchants to integrate. From technical community feedback, agent developers indeed need cross-border payment, especially for scenarios like SaaS tools, AI assistants, and intelligent customer service, where users are global and payment is unavoidable.

Differences from Domestic AI Payment

Alipay’s domestic AI payment system is already complete: AI Pay (agent-initiated payment), AI Receive (merchant agent receiving payment), AI Wallet (user managing agent authorization), and Token Pay (large model provider recharge solution). This approach works domestically because Alipay is already the infrastructure, user trust is high, and regulation is clear.

But going global can’t simply copy this. No single payment platform internationally holds the monopoly Alipay has in China, and user payment habits are highly fragmented. AMP is positioned as a “connector” rather than a “replacement” — not to get all global users to use Alipay, but to let local wallets connect to the agent commerce ecosystem through AMP.

This thinking continues the Alipay+ logic: essentially an aggregation gateway that connects different countries’ e-wallets so Chinese tourists abroad can use Alipay and overseas visitors to China can use their local wallets. AMP extends this logic to AI scenarios — regardless of the wallet you use, once it integrates AMP, agents can help you complete cross-border payments.

Another difference is the security model. Domestic AI payments rely on Alipay’s real-name system and risk control engine — user identity is trustworthy and transaction flows are transparent. International markets are much more complex — KYC (Know Your Customer) standards differ across countries, as do data privacy regulations and dispute resolution mechanisms. AMP must achieve traceability while protecting privacy — a technical challenge and a compliance requirement.

Ant International’s approach is to use privacy computing technology (MPC, homomorphic encryption) to embed verifiable credentials into the flow, meeting privacy regulations like GDPR while still providing evidence in case of disputes. If successfully implemented, this methodology could be a reference for the global payment industry — trust mechanisms in the AI era are fundamentally different from traditional payments.

Competitive Landscape

AMP is not the only agentic payment protocol. Mastercard’s Agent Pay and Visa’s Intelligent Commerce are doing similar things — but their entry point is credit card networks, while AMP focuses on e-wallets and alternative payment methods (APMs).

From a market share perspective, credit cards dominate in Europe and North America, but e-wallets and local payment methods are more popular in emerging markets such as Asia-Pacific, Latin America, and the Middle East. Ant International’s advantage is its established wallet network in Asia-Pacific — AMP can quickly tap into these existing resources. Mastercard and Visa, while stronger brands, lack local payment infrastructure in these regions.

Another variable is the alignment of AI large model providers. If top players like OpenAI, Anthropic, and Google choose to partner with Visa or Mastercard, AMP’s rollout will face obstacles. However, disclosed information suggests Ant International is already working with Google on a “universal commerce protocol” that integrates the entire AI shopping process — meaning they are at least partners in some scenarios.

Chinese large model providers going global are potential AMP customers. MiniMax, Step Star, and Zhipu AI have already integrated Alipay AI payment domestically; if their products expand internationally, AMP offers an out-of-the-box solution. This mirrors how Chinese internet companies once used Alipay for overseas payments — except now the main actors are AI applications instead of e-commerce platforms.

Barriers to Deployment

To achieve large-scale commercialization, AMP has several hurdles to overcome.

First, standardization. Mobile payment protocols only gain value when enough players adopt them. If only wallets in Ant International’s ecosystem integrate, AMP remains a private protocol without network effects. Ant International must convince more independent wallet platforms, payment gateways, and merchant service providers to join, which requires time and careful design of profit-sharing mechanisms.

Second, regulatory compliance. Cross-border payments involve anti-money laundering (AML), foreign exchange controls, and consumer rights protection, with vastly differing policies among countries. AI agent payments, being new, lack clear legal frameworks in many regions. If regulators in some markets take a cautious stance toward agent-initiated transactions, AMP’s adoption will be limited.

Third, technical maturity. Agentic payments rely on large models’ intent interpretation capability, but current models’ accuracy in complex payment scenarios is still insufficient. For example, if a user says “Book me a flight to Seoul tomorrow, economy class, morning,” can the agent accurately understand what “morning” means? If it misinterprets and buys an unwanted ticket, how is responsibility assigned?

AMP’s verifiable credential mechanism allows for retrospective checks, but it cannot fundamentally prevent operational mistakes. Large model providers need to impose more product-level constraints, such as requiring manual confirmation for high-value transactions or secondary verification for sensitive actions. The protocol can provide these capabilities, but whether they are used depends on application developers.

Finally, user education. The concept of agentic payment is unfamiliar to most people, especially in cross-border contexts, where trust in AI spending money on the user’s behalf is lower. Ant International must work with wallet platforms and merchants to gradually build user habits through small, low-risk scenarios (like topping up phone credit or buying coffee) before pushing large cross-border transactions.

Points Worth Watching

Alipay+ GlassPay. This essentially embeds payment capabilities into smart glasses, using iris + voiceprint for “pay at a glance.” Ant International is piloting this with Xiaomi and Xingji Meizu in ride-hailing and cross-border consumption scenarios. If smart glasses become the next computing platform, GlassPay combined with AMP could enable “see it, buy it” — far superior to current voice assistant payment experiences.

AI Merchant Agent ‘Xiaoyu’. In China, Alipay has launched a store-level AI partner that integrates payment, membership, product, and traffic distribution capabilities. If this model is replicated in overseas markets with AMP, small and medium merchants could connect to the global payment network at low cost — significantly impacting cross-border e-commerce and local services.

Open-source strategy. Antom’s open-sourcing of the agent payment solution on GitHub clearly aims to capture developer mindshare and make AMP a de facto standard. If the open-source community accepts the solution, other payment providers, even if reluctant, may need to consider AMP compatibility to avoid marginalization.

Ties with large model providers. MiniMax and Step Star have integrated Alipay AI payment domestically; if they continue to use Ant International’s solution overseas, AMP will have seed users. The key is whether it can win over international players like OpenAI, Anthropic, and Google — which would determine AMP’s global influence ceiling.

Final Thoughts

AMP is essentially Ant International’s strategic positioning move in the AI agent economy era. In payments, whoever controls the protocol standard controls the ecosystem’s discourse power.

From a business logic perspective, Ant International’s approach is “build roads, collect tolls” — not making wallets or handling user funds but connecting the global payment network and taking a cut from transaction flows. The benefit is light operation — avoiding licenses and localization in each market — but the drawback is dependence on partners; if wallet platforms don’t buy in, the protocol is just a castle in the air.

Agentic commerce is still in its early stages, and payment is just one link. Why should users trust AI to spend money for them? Why should merchants accept agent-placed orders? Why should large model providers share revenue? There are no standard answers. AMP’s success depends not only on advanced technology but also on Ant International’s ability to coordinate interests and turn the ecosystem.

At least for now, Ant International has one advantage over others: it has already run the model domestically, knows which pitfalls to avoid, and where to invest. If this experience can be replicated overseas, AMP has a chance to become the standard protocol for agentic payments.

But the window of opportunity won’t stay open long. Visa and Mastercard are moving, and Stripe and PayPal won’t stand by — each wants to stake a claim in the new agentic payment track. Ant International must expand AMP’s ecosystem before competitors react; otherwise, no matter how good the protocol is, it will be playing alone.

References

- Ant Group Launches Overseas AI Payment Solution - 36Kr — First disclosure of AMP protocol release

- Ant International Advances: From Cross-Border Payment to Agentic Payment - CLS — Detailed introduction to Ant International’s Alipay+ business layout and data

- Supporting Global AI Economic Development: Ant Offers Global AI Payment Solutions - Xinhua News — Official release of Alipay’s domestic AI payment ecosystem

- Ant International’s Antom Releases AI Agent Payment Solution - Antom Official Site — Technical details and security mechanism of AMP protocol

- Ant Group CEO Han Xinyi: Built a New AI Payment Service Adapted to Agentic Commerce - The Paper — Official statement on Ant Group’s AI payment strategy