Visa puts its payment network into ChatGPT, and AI agents can finally pay on their own

Visa announced that it will embed its global payment network into the OpenAI platform. With user authorization, ChatGPT can independently complete the entire shopping process from search to payment. This is a key step for OpenAI to re-enter intelligent agent e-commerce, following the setback of Instant Checkout three months ago.

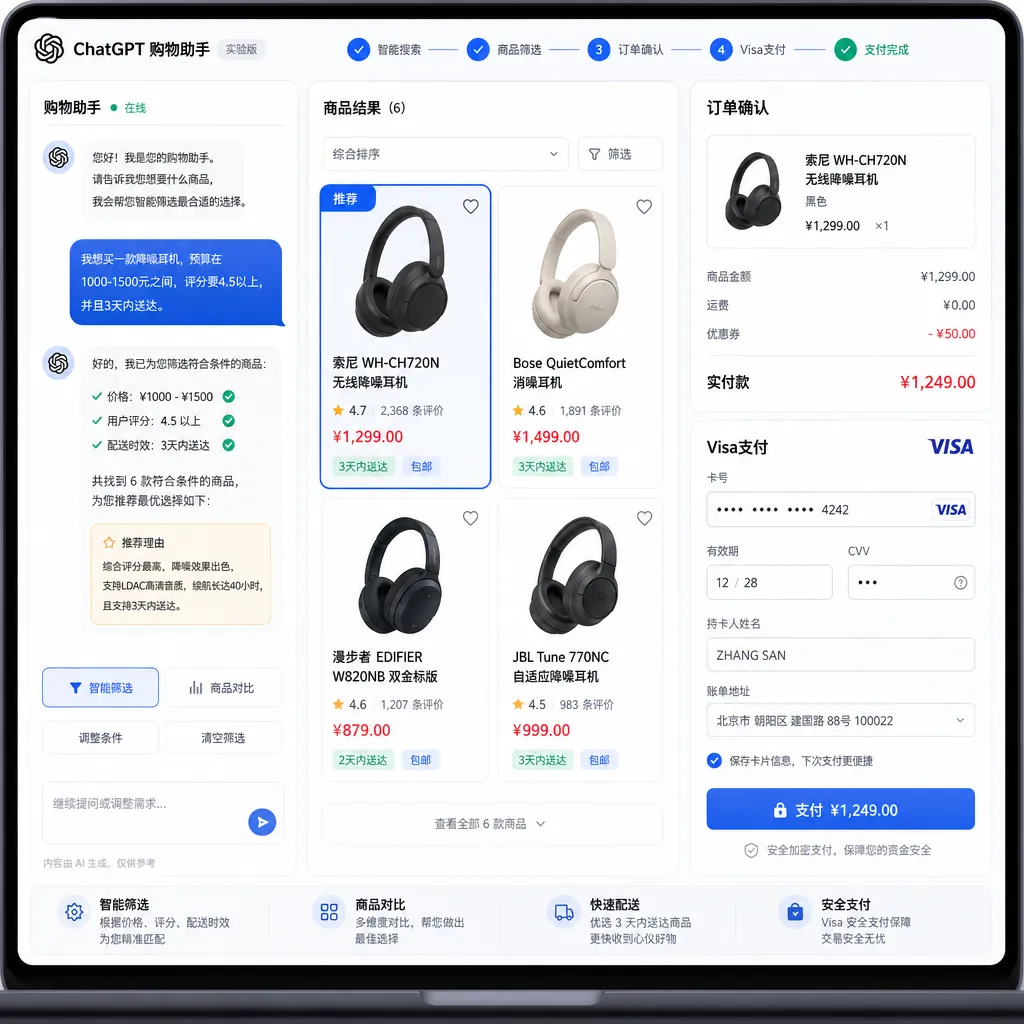

On Wednesday at the Visa Payments Forum in San Francisco, Visa announced a strategic partnership with OpenAI to embed its global payment network directly into the OpenAI platform. Translated into developer-friendly terms: in the future, once you give authorization, ChatGPT will be able to charge your Visa card on its own to buy things for you—handling everything from search, price comparison, ordering, to payment confirmation—without you having to click “Confirm” again.

This is another major move from Visa this year after collaborations with Anthropic and Microsoft. But unlike the previous two, which stayed at the exploratory agreement level, this time they’re actually aiming to run a complete transaction loop inside the biggest AI entry point on the consumer side.

1. What happened: the “$150 wireless headphones” demo

At the forum, Visa executives showcased a very straightforward scene: the user says to ChatGPT, “Find me a pair of wireless headphones under $150,” the model screens candidates, the user clicks confirm, and the rest—placing the order, charging the card, verifying the shipping address—is all handled by the AI agent. From the merchant’s side, what they receive is a transaction initiated by an AI agent but processed through Visa’s standard clearance network.

This means two things:

- The AI assistant’s role has been upgraded from “recommend” to “execute.” Previously, ChatGPT could at most produce a shopping list, and you’d still have to manually go to Amazon or Shopify to check out. Now that step is removed.

- The payment integration now covers all online merchants that accept Visa. Merchants don’t need to sign a special integration agreement with OpenAI; if they accept Visa, theoretically they can take an AI agent’s payment.

Visa’s Chief Product & Strategy Officer Jack Forestell said at the forum, in words that might sound flashy but ring true: the changes AI will bring to commercial activity will be more profound than those from the Internet and mobile Internet eras. Their focus is to ensure transactions initiated by AI agents are “trustworthy, secure, and smooth.”

2. Why now: after Instant Checkout’s failure

You can’t really talk about this collaboration without mentioning a slightly embarrassing backstory.

In late 2025, OpenAI launched a feature called Instant Checkout, based on its self-developed “Agentic Commerce Protocol,” in partnership with Stripe, initially supporting Etsy and over 1 million Shopify merchants. The pitch was: users could click “Buy” within ChatGPT when seeing a product, confirm order, address, and payment details without leaving the chat interface.

It sounded great. But it only ran for a few months.

In March 2026, Instant Checkout quietly went offline. Industry postmortems identified two main reasons for failure:

- High transaction error rate. The AI agent had higher failure probability than traditional e-commerce in order matching, inventory confirmation, and address verification. Refunds, customer complaints, and reconciliation costs got pushed onto merchants.

- Merchants disliked the commission model. OpenAI charged a small fee per order, but merchants’ logic was simple: how certain is the GMV you bring me? Do you have conversion rate data? If not, don’t expect to take a cut. Among over 1 million Shopify merchants, only a few actually ran it.

So Visa’s involvement this time is not just a nice addition—it’s actually solving problems.

3. What Visa brought to the table

Visa isn’t providing a new payment UI—they bring an entire clearing, risk control, and compliance infrastructure that’s been running globally for decades. In the context of agent-based e-commerce, they mainly solve three issues:

1. Merchant acceptance

Instant Checkout’s fatal flaw was merchants needing to “actively integrate” OpenAI’s protocol. Now it’s: as long as a merchant already accepts Visa, AI-agent-initiated transactions follow the exact same clearance path as regular online transactions, without needing to change a single line of code for AI. This drops the integration threshold from “do BD with OpenAI” to “do nothing.”

2. Fraud & tokenization

Visa provides tokenization, instant authorization, and fraud monitoring. AI-initiated transactions carry a special identifier, allowing merchants and issuers to recognize “this was done by an AI agent, not directly by the user,” enabling distinct risk control strategies.

This is actually key to agent-based e-commerce. Think about it: if you link your card to ChatGPT and the model glitches and makes ten purchases, who’s responsible? Previously, such disputes were unsolvable—issuers didn’t know whether it was user-authorized or just model malfunction. Tokenization plus transaction identifiers at least define the boundaries of responsibility.

3. User-side control

Visa and OpenAI clearly stated: transactions will operate within user-set spending limits, approval thresholds, and merchant whitelists.

For example, you can tell ChatGPT: “Ask me for approval for any single purchase over $200,” “only buy from these 20 merchants,” “monthly budget not over $1000.” This essentially brings traditional credit card virtual card/limit card functions into the AI authorization layer.

4. Racing with Mastercard and PayPal

This isn’t just Visa’s game. Mastercard already introduced Agent Pay, and PayPal is discussing similar partnerships. Google’s “AI shopping mode” already supports agent checkouts, all in-house.

But OpenAI is special—ChatGPT’s consumer-side recognition and weekly active users (officially 700 million weekly) could surpass all other AI entry points combined. Securing this position means Visa has locked the largest traffic pool at the AI payment entry point.

The secondary market reacted accordingly: after the news, Visa’s stock price rose about $3, though it still closed down 0.47% at $323.47 due to broader market decline. Relative to NASDAQ’s nearly 2% drop that day, this was quite resilient.

This is the first time industry predictions of AI agents potentially handling about one-fifth of e-commerce transactions within a year have a solid practical path.

5. Developer perspective: is the Agentic Commerce Protocol still alive?

Here’s a detail developers should note: OpenAI’s previously open-sourced Agentic Commerce Protocol (ACP)—the tech backbone of Instant Checkout—has not been abandoned.

Based on current public info, the new Visa integration looks more like an extension of ACP’s Delegated Payment spec, using Visa’s tokenization as an officially supported payment credential mechanism. Merchants already integrated with ACP theoretically don’t need to re-integrate—just have another payment option.

Some key ACP design principles still stand:

- Merchants control the orders. ChatGPT just passes messages; accepting/rejecting orders, deducting inventory, and fulfillment remain in the merchant’s system.

- Payment processors aren’t tied to Stripe. Stripe is the reference implementation, but merchants using other processors can still integrate—via Stripe’s Shared Payment Token API or ACP’s Delegated Payment spec.

- AI agent’s identity is “user’s shopping assistant.” Not a merchant sales channel, so ChatGPT has no incentive to promote specific products (official line says product ranking isn’t influenced by Instant Checkout support, but we’ll have to see).

PSPs like Checkout.com have stated they’ll join in, co-building the tokenization framework with Mastercard and Visa. Expect within the next 6–12 months, “agent payment” will be a must-have feature for major PSPs—without it, they risk falling behind.

6. Problems still unresolved

Let’s cool the hype a bit. This looks shiny, but there are at least four unaddressed pitfalls:

1. Is the model’s “shopping judgment” good enough?

If you ask ChatGPT for wireless headphones under $150, will it choose Sony WF-1000XM5 or a random brand? The biases, mistakes, and ad pollution in that decision (even if officially there’s no paid ranking) translate directly into cash losses. Instant Checkout’s high error rate wasn’t a payment issue—it was the model’s shopping intent comprehension still lacking. Visa can’t fix this.

2. Return and customer complaints process?

When the product isn’t satisfactory, do you return it via ChatGPT or the merchant? What role does the AI agent play in after-sales? No clear answer yet.

3. Privacy and data ownership.

Your shopping preferences, address, payment habits now live between ChatGPT and Visa, with both holding copies. Defining the data-sharing boundary—especially under EU GDPR and California CCPA—will be a major tug-of-war in the coming year.

4. Risk of AI “being planted” for recommendations.

Technically tricky: can merchants manipulate product ranking in ChatGPT’s recommendations via SEO-like methods? Past term was SEO; future might be AEO (AI Engine Optimization). Once this gray industry chain kicks off, “unsponsored, natural ranking” promises will quickly sour.

7. Meaning for Chinese developers

In the short term, Visa+OpenAI’s agent payment capability will be mainly US-focused. But once the agent-based e-commerce paradigm is established, Chinese AIs (Doubao, Kimi, Tongyi, DeepSeek) and domestic payment networks (UnionPay, Alipay, WeChat Pay) will likely follow with their own versions.

For developers, two things to watch early:

- Open-source implementation of the Agentic Commerce Protocol (ACP). OpenAI has confirmed they’ll open-source it, and it could become a de facto standard.

- “Payment tool” abstraction in Function Calling and Tool Use. In future, your agent won’t just have search or weather functions—it’ll have “order,” “pay,” “track logistics.” Designing permission boundaries for these tools will be a new challenge for agent development.

On a side note, OpenAI Hub already supports calls to the latest GPT models. Developers wanting to build agent demos with shopping capability can directly use one API key to connect GPT, Claude, Gemini, DeepSeek for comparison testing—saving the hassle of registering multiple accounts.

8. In closing

AI can chat, code, draw, and do research—those are still “information processing.” But when AI can take out your wallet and pay, it shifts from “tool” to “participant in economic activity.” This is far more significant than releasing a GPT-5.5.

The real meaning of Visa and OpenAI’s collaboration isn’t “ChatGPT can shop now” but that it has paved the critical part for agent economics—trust and settlement. The rest depends on when the model’s judgment can match the reliability of the payment network.

This battle has only just begun.